I Sell IULs NOT’ FOR WHAT THEY MIGHT DO…

But For What They Are Contractually Guaranteed To Do!

Starting in Charlotte NC in 1996 & now based in Durham, NC since 2007, we’ve been providing professional Insurance & Retirement Planning for thousands of businesses, non-profit entities and individuals!

Free Consultation

919 – 519 – 2721

The Era Of IUL

So What Are The Contractual Guarantees?

In my opinion, the first job of an IUL is to provide “Asset Protection” by way of providing key, contractually guaranteed benefits.

The most well-known use of an IUL is for tax-free retirement income however this method isn’t guaranteed (but then again neither is your stock market portfolio). This method centers around max-funding the policy within 5 years.

(Hint* Hint* If you have a So-called Bank or Life Insurance Retirement Plan or “Rich Man’s Roth” and the premiums stretch beyond 5 years…. there’s a good chance it’s not set up correctly!

Disclaimer Alert* I’m a strong advocate for Max-Funding An IUL or Whole Life but only after pre-requests have been met.

In the next section I’ll explain what my pre-requests to max-funding an IUL are (which by the way will exclude the majority) but first let’s talk about the contractual guarantees for asset protection and why you need to purchase an IUL today!

1. Guaranteed Premiums

2. Guaranteed Death Benefit

3. Guaranteed Living Benefits

4. Guaranteed Lifetime Coverage

5. Guaranteed Cash-Out Option (Return Of Premium)

Note: If you would like a copy of my IUL Mystery’s Myths & Facts Explained report…which dives into the “Cash Accumulation Component” of IULs, click the “Contact” tab at the top.

Inspired By A Social Media Influencer.

A very popular social media influencer made this comment:

*****”The VAST majority of people don’t need a permanent life insurance policy aka “cash-value life” Instead purchase a 20-year term policy and make sure you purchase one that gives you the ability to renew it” Just in case you still need coverage and your health takes a turn for the worst.”*****

This website will set the record straight on Permanent Life insurance aka cash-value life aka whole life aka UL aka IUL!

For the record I recommend them all: Term-Whole Life-IUL depending on the needs of the client. One isn’t better than the other as they each have different proposes for different situations and your personal situation is unique to you!

Let’s begin, with the first contractual guarantee.

The obvious one first: The Guaranteed Death Benefit!

Technically no one really talks about the guaranteed death benefit as most IULs aren’t sold for the death benefit but for the cash accumulation value.

With my favorite IUL I can guarantee the death benefit from age 96 up to age 121.

This is “KEY” because you’ll hear most whole-life agents, buy term and invest the difference reps and so-called financial gurus falsely claim you don’t have a guaranteed death benefit with IUL.

Th

These claims are 100% wrong because with my favorite IUL this benefit is a contractual guarantee.

*NOTE*

Typically when trying to prove a point, most people will pick the absolute worst feature of a product as their “WHY”. For example:

You can have 10 different whole life / cash-value life insurance policies all with 10 different features.

The anti-whole life or anti-IUL person will reference a troublesome feature with (ONE) out of the 10 products and use this one example as to why they don’t like any whole life or IUL plan.

Is this method of determining the worth of a product legitimate?

The answer is NO!

******

There’s a CFP-Certified Financial Planner of 45 years in my local market with a weekend radio show.

On air, he told a caller he doesn’t like annuities because when you die the insurance company keeps your money.

Out of the 100+ different customizable annuities on the market, he decides to use the only annuity type on the market that actually keeps the money when you die.

But what about the other 99 out of 100 annuities that do pay the remaining balance to your beneficiaries?

Why are you using the 1% for your example instead of the 99%?

The other very important part of this particular annuity is this:

The client has to choose this option, however very few do!

If a client doesn’t have any family, friends or charity organizations they would like to leave an inheritance too, the option of allowing the money to remain with the insurance company is chosen.

The “KEY” takeaway is this… You have to select this option, the insurance company doesn’t choose this option on your behalf. It’s your decision to make.

When you look at annuity sales data, you’ll find this type of annuity (with no payout to beneficiaries) equals less than 1% of all annuities sold.

Individuals purchasing this seldom-used annuity do so because they have no family, friends, or charity organizations to provide for.

The other 99% of individuals purchasing an annuity, provide for the remaining balance to flow to their beneficiaries.

I mention this because the “So-called Financial Gurus” you see and hear on TV / Radio are guilty of the same thing when it comes to explaining why they don’t like cash-value life insurance.

The “Anti-Cash-Value Life” crowd always picks the worst-case scenario as their example.

In 28 years I’ve never had anyone provide me with a true comparison as to why cash-value life isn’t a good idea lol.

There’s always a “WHY” concerning various financial products & it’s my job to explain the “WHY” behind cash-value life.

The “WHY” behind my favorite IUL with contractually Guaranteed Asset Protection Benefits!

Premiums Are Guaranteed For Life

Critiques of cash value life always talk about the cost of insurance reaching unbearable limits when you get older during a time you can least afford to have increasing premiums.

YES! They say your premiums will increase when you get older due to the cost of insurance increasing.

The funny part of this argument is this: They’re actually explaining what will happen to your term life insurance if you find yourself in a situation needing to renew it. lol! They’re just clueless and don’t know it!

With whole life insurance 99.9% of the plans have guaranteed level premiums. The key word is, guaranteed level premiums.

The only reason why the premiums would increase on a whole-life policy is if you borrowed money from the policy with a low cash value balance without paying it back.

Removing money from a policy that isn’t a max-funded policy will almost always trigger a letter from the insurance company asking you to pay the money back or increase your premiums.

If you only make the minimum premium payments, the cash value will also be minimal.

With a UL / IUL policy, you have options when designing the plan.

You can create a Universal Life policy with a premium only designed to carry the policy for 10 years.

The trick these Gurus and buy term & invest the rest people will do is this.

They’ll find a Universal Life policy designed with a premium that will allow the policy to last 10 to 20 years “only” before it lapse.

They’ll use this example to prove why cash-value policies don’t work lol…

But the real reason why this particular design will lapse after 10 or 20 years is because that’s how it was set up lol.

You can set a Universal Life policy to only last 10 years, from 20 years to age 96 to age 100 to age 105 to age 110 even to age 121.

You have the flexibility to set the expiration of the policy based on the needs of the client.

An illustration showing a policy lapse after 10 years isn’t a defect in the policy.

It’s simply the way the agent or advisor set it up!

My favorite IUL wins the day with Guaranteed Premiums to age 121.

This is a “Contractual Guarantee”

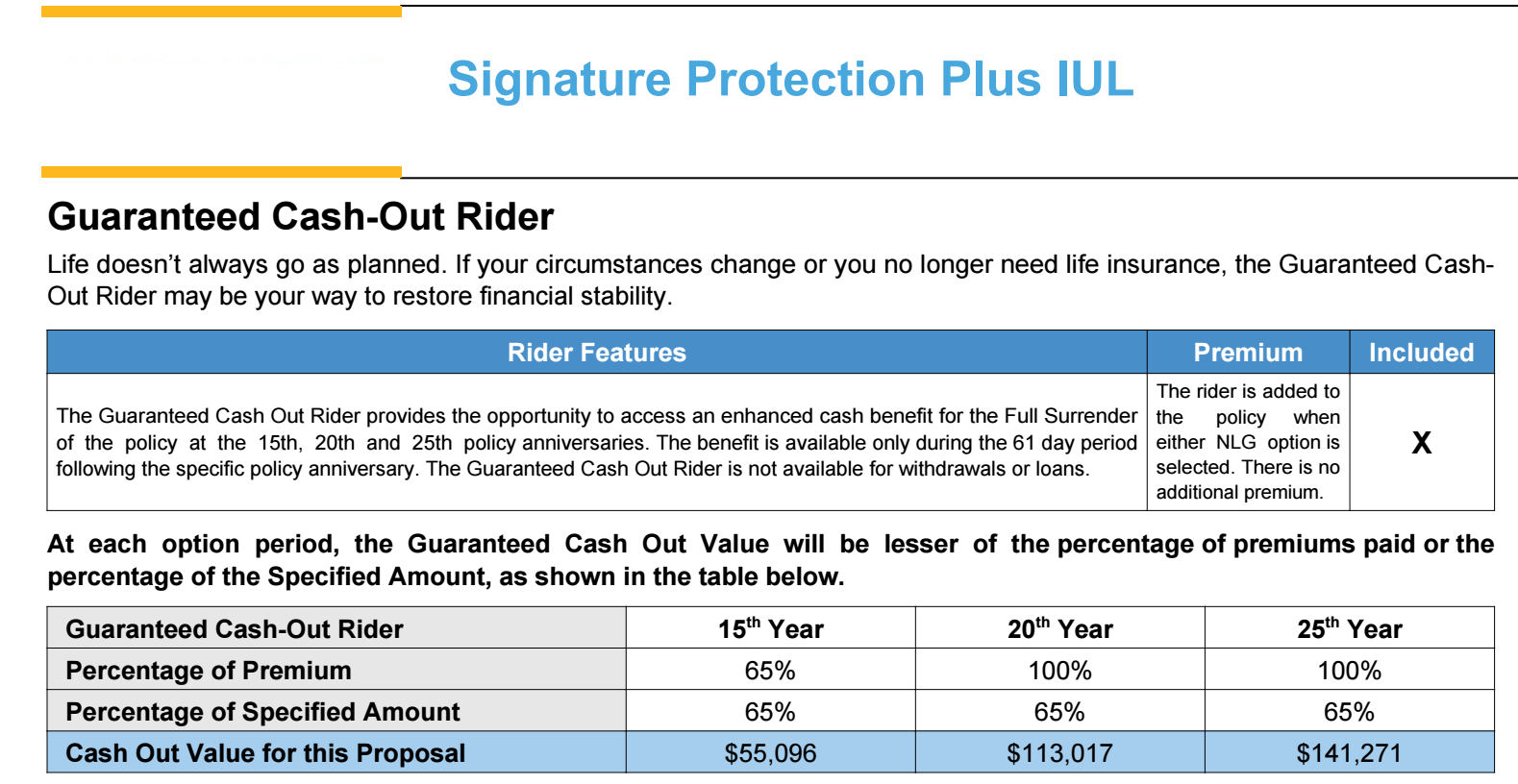

Guaranteed Cash-Out Option.

The “Guaranteed Cash-Out Option is a different twist for an IUL product.

This feature just speaks to the versatility of Universal Life Insurance products.

Not every IUL has a GCO!

If after 15 years you decide the policy is no longer needed you can opt for a 50% Guaranteed Cash-Out.

Wait 5 more years and receive a 100% cash-out in year 20.

In year 25 you’ll be offered one more opportunity to cash out at 100%.

This benefit is “Guaranteed”

With a typical 20-year term policy, if your health took a turn for the worst and you wanted to renew the term policy instead of trying to purchase a new term policy…..

The premiums could increase by over 1,000%

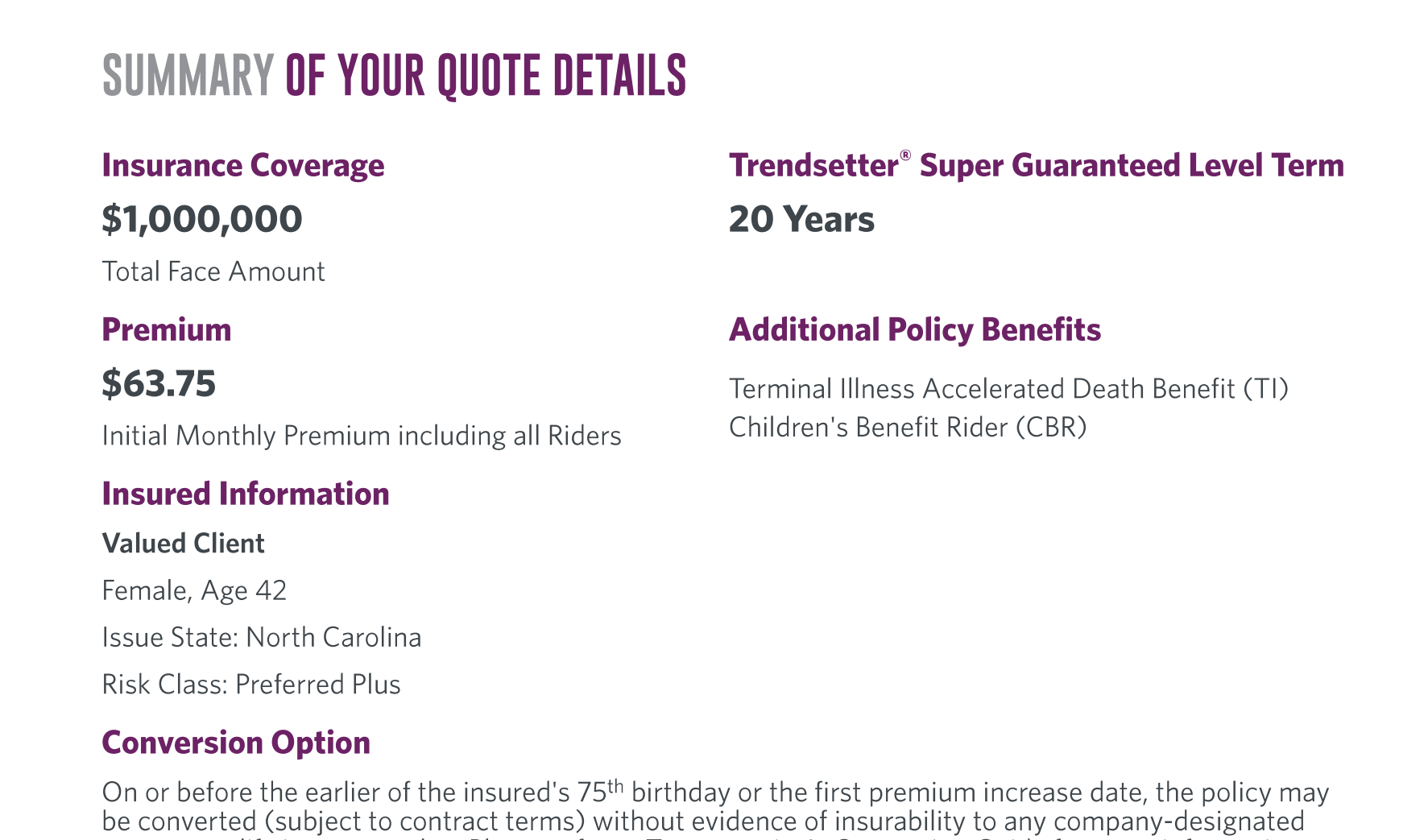

For example, if you had a 1 million 20-year term policy with a premium of $63.75 per month.

Instead of purchasing a new term policy, you decide to renew the same policy because you developed serious health conditions that could prevent you from qualifying for a new term.

While it’s great most term policies will allow you to renew at the end of the term without proof of insurability…. Only a few can afford to do so!

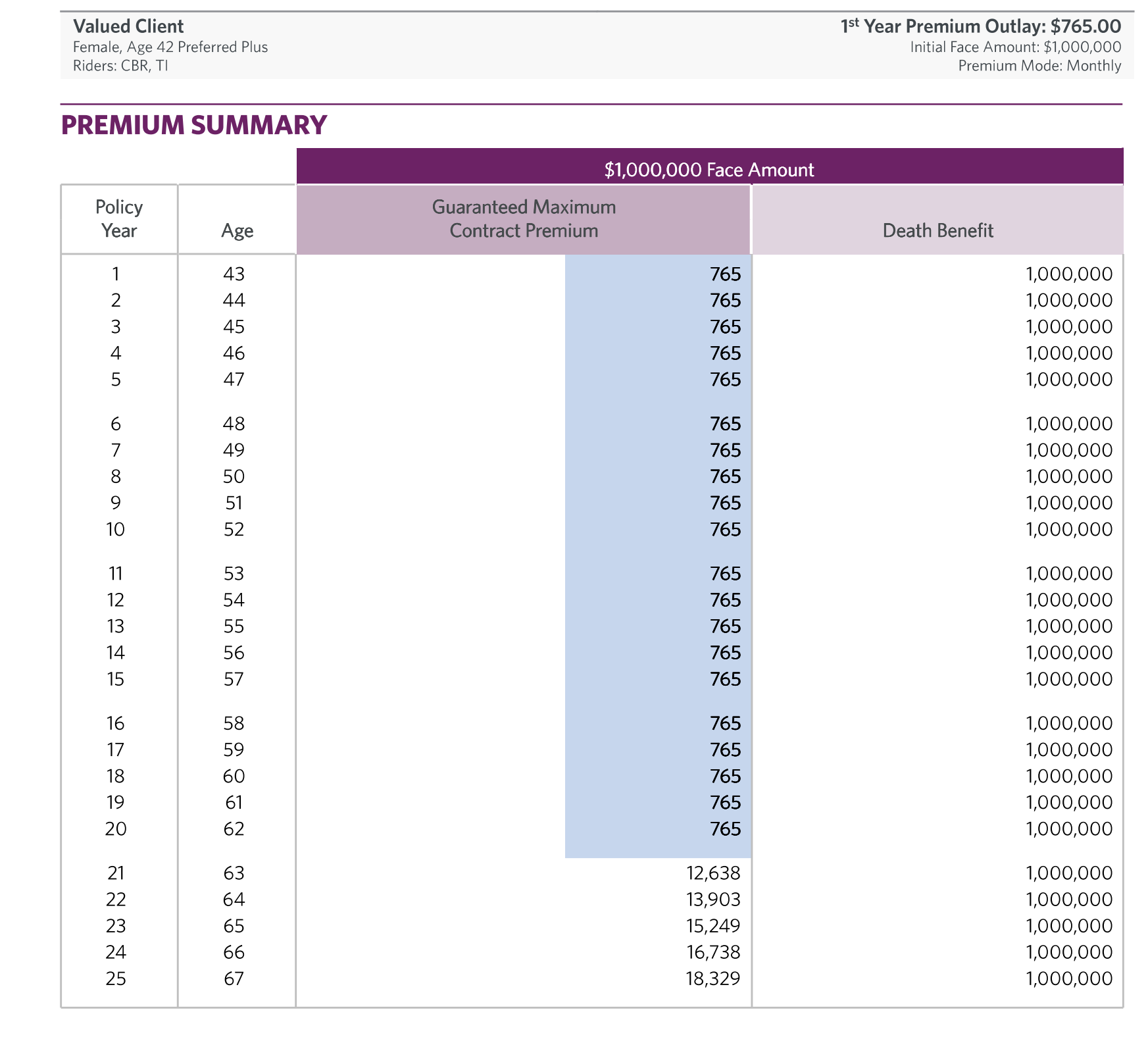

The 1 million 20-year term policy at $63.75 per month jumps to a monthly premium of $1,053.16 starting in year 21.

The premiums will continue to increase every year….some plans will increase premiums every 5 years before switching to increasing every year.

With this example, the monthly premium for year 21 is $1,053.16

By year 30 the monthly premium is: $2,246.58

By year 41 at age 83 the monthly premium is: $9,140.08 (Annual premium of $109,681)

I always hear Buy Term & Invest The Rest Agents/Advisors promoting “Term To Age 95”

My only question is… who in their right mind will continue paying for a term policy renewing every year to age 95?

With this same plan by year 50 (Age 92) the annual premium is $309,992.

Can you imagine someone trying to pay $25,832.66 per month at age 92?

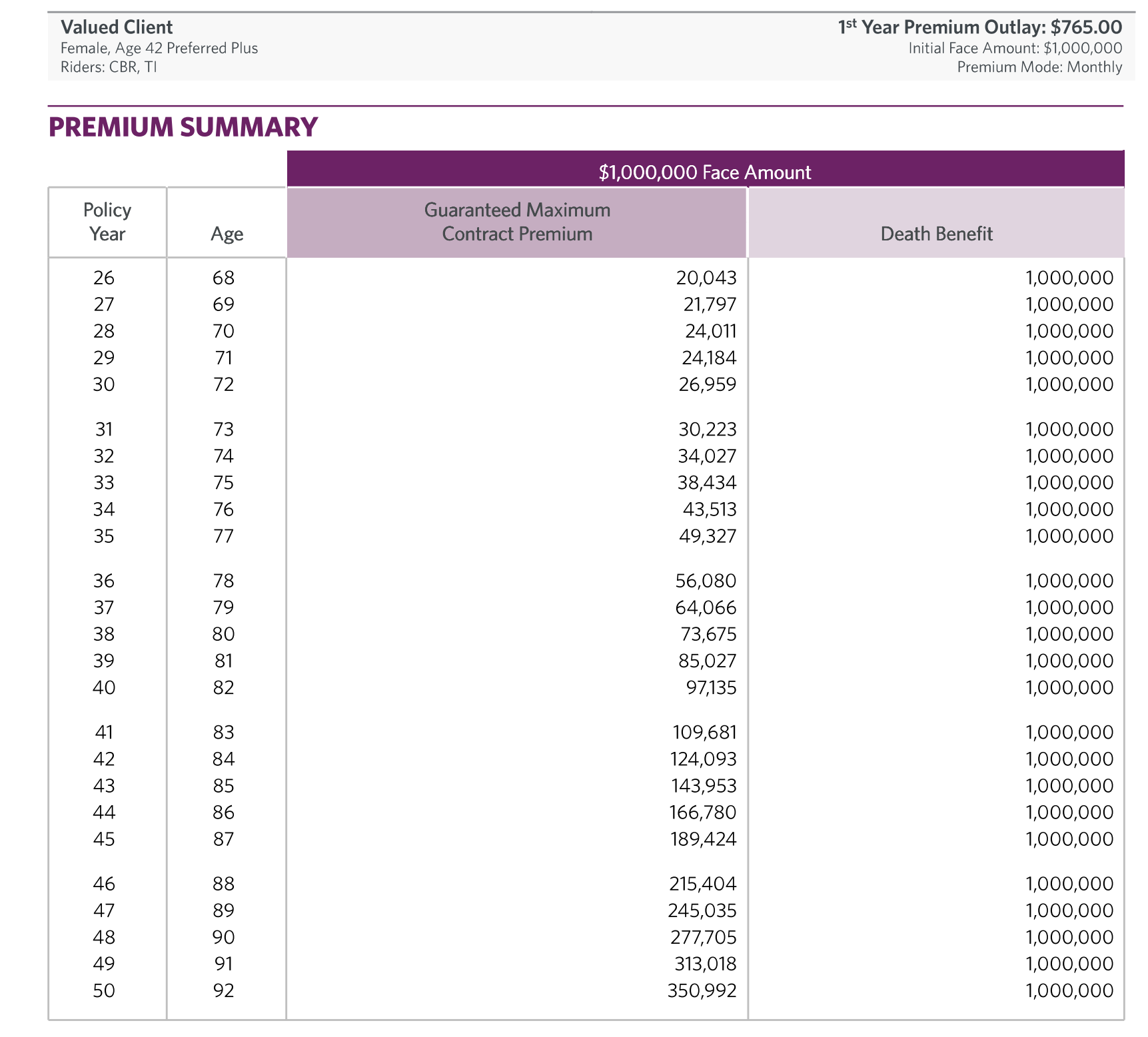

By year 96 the annual premium is a whopping half million plus – $530,818!

The total premium for this term to “96” is $4,754,181. Almost $5 Million for 1 Million of coverage lol.

When the insurance company keeps the money it’s because the

One of the main reasons for purchasing a life insurance policy is for the unknown….

Why would you recommend only purchasing a term policy when your future financial situation is unknown…. when your future health status is also unknown?

The answer is YES!

A permanent life insurance policy will cost you way more starting off, however over the term of your entire life, the guaranteed premiums of a permanent life insurance policy will cost you way less!

Guaranteed Cash-Out Option. Part 2

Compare the price of this term policy to my favorite IUL for $1 Million dollars of life insurance coverage.

The premium starts off much higher than the term policy.

$1 Million 20-year Term starts off at: $63.75 per month.

$1 Million IUL (w/Guaranteed Premiums) starts off at $470.91 per month

With this IUL example, the premiums are guaranteed to age 96 however I can guarantee the premiums to age 121.

(Just in case you’re wondering…The guaranteed premium to age 121 is $533.29)

The IUL premium in this example stays the same and never increases.

By age 96 (54 years later) the total premium paid for $1 Million dollars of life insurance coverage is: $305,154.

By age 96 (54 years later) the total premium paid for $1 Million dollars of Term life insurance coverage is a whopping 4 Million plus….:$4,754,181!

I have a new suggestion!

Instead of “Buy Term & Invest The Rest” how about “Buy (Perm) & Invest The Rest” lol

If you think by age 70, 75, 85, or 95 you’ll still be in perfect health…. only purchasing a term life policy would be the way to go.

If there is a possibility you will not be in perfect health… a permanent policy might be the way to go.

No one can predict the future however the data shows 89% of Americans 65 and older are taking some kind of prescription drug!

This tells me the overwhelming majority of people will not be in perfect health by the time their term life insurance policy is up for renewal.

A recent CMS study showed that 70% of current 65-year-olds will need some kind of long-term care services.

Please don’t listen to these Gurus” telling you not to purchase a permanent policy…

Every possible research known to man points to securing a permanent life insurance policy when you are young and keeping it your entire life.

Research shows the overwhelming majority of Americans are unable to self-insure after reaching retirement age…and as a result, end up having to purchase a 10k Final Expense policy for the same price of $250,000 permanent policy if purchased at a younger age.

Over the last 10 years, I’ve personally spoken with thousands of individuals over the age of 65 having to settle for $10k of life insurance because their term life insurance policy expired and they couldn’t afford the renewal premiums and can no longer qualify for the best health underwriting for a new policy.

These individuals are forced into paying for high premium-small death benefit life insurance plans.

WHY!

Because someone told them to buy term insurance only!

I personally think these individuals should be held accountable for their bad advice.

I along with thousands of agents & advisors are literally in the trenches working with the 10,000 plus Americans turning age 65 every day who are unable to afford the renewal premiums on the term policies, unable to self-insure, unable to afford a policy over 10,000!

Buy Term & Invest The Difference has created an entire group of Americans 50 million strong, retired, and still in need of life insurance.

No one knows the curve balls life will through them….this is why i recommend getting a permanent life insurance policy at the youngest age possible to lock in the rate for your future self.

****

Permanent Life Insurance Plans also have living benefits to help pay for chronic & long-term care services.

It’s like having a 5 for 1 policy.

A female age 30 in good health can purchase my favorite IUL policy for $250,000 of coverage providing up to $200,000 for long-term care services.

If kept till age 90 the policy would cost $65,520.

A female age 60 (assuming good health) purchasing a “Long-Term Care Policy” till age 90 will spend $139,345 providing for, $184,000 of long-term care services.

Don’t need to be a mathematician to figure out which option might be best!

A permanent cash-value policy (IUL) purchased at an early age will not only end up costing less than a Term Life Insurance Policy To age 95 but it can potentially save you over $100k in future Long-Term Care Premiums.

If in this example you die at age 90 without ever needing long-term care services…with the cash value IUL policy your beneficiaries would receive an income-tax-free death benefit.

If you spend over $100K (any amount) for a long-term care policy and you die at the age of 90 your beneficiaries get nothing.

When you factor in “Life Insurance” as an Asset Protection Tool & not just for the death benefit, the “Buy Term Only” scenarios begin to look very bad!

Right Now I can hear all of my “Buy Term Only Advisors” yelling in my ears saying the **invested difference will allow you to self-insure.** lol (Are You Sure About This?)

In the next segment, we’ll once and for all find out if this is true!

*Spoiler Alert:*

Over the last 28 years I’ve challenged thousands of advisors to provide me with ONE example of an actual client who was successful with implementing the Buy Term & Invest The Rest strategy and as a result was able to be self-insured by the end of the term.

And I’m still waiting!

The "Invested Difference Will Allow You To Be Self-Insured? True Or False?

Buy Term & Invest The Difference sounds really good.

Question:

Do you know anyone personally who’s actually proved to you on paper, that this strategy has worked as planned?

It’s literally impossible for it to work.

Unless my calculator is broken, it’s literally impossible for you to replace your life insurance death benefit by only investing the difference between the cost of a term policy and the cost of a permanent policy…. by the time your term policy is up for renewal.

The trick with this comparison as used by the buy term only people is this:

They’ll use some crazy ridiculous whole life insurance quote of someone receiving a deathbed life insurance quote versus a term life quote for a marathon runner. lol

This is hardly a true comparison…. of course, the rates are going to look way different if this is your comparison.

Let’s look at an honest comparison.

*********************************

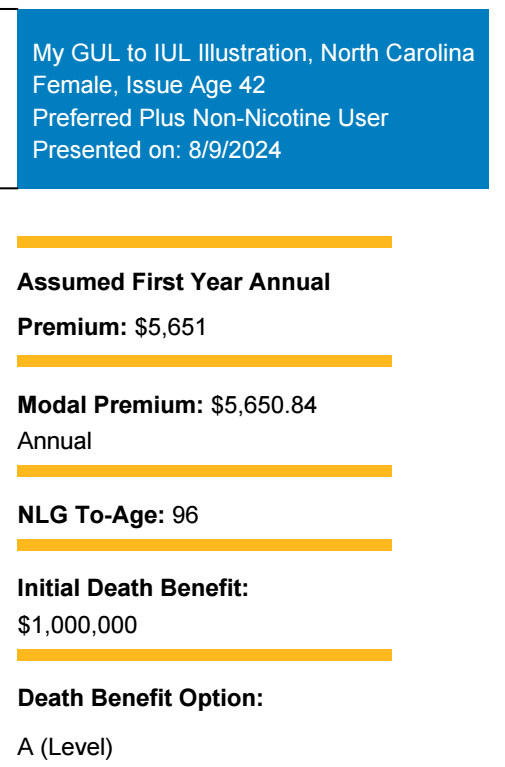

I will compare a term life preferred plus rate with a cash value life insurance preferred rate.

Female Age 42 nonsmoker $1 Million in coverage.

I’m tilting this scenario towards the term life side because I’m using a high death benefit.

The difference in premium between a $250k 20-year term & a $250k cash value life policy isn’t as significant as comparing a $1 Million 20-year term versus a $1 Million cash value life.

So for this example, I’ll use the higher costing 1 million cash value life.

The spread is much larger when using a much higher death benefit.

$1 Million 20-year Term:

$63.75 ($765 a year)

$1 Million Cash-Value Life:

$471.75 ($5,661 a year)

A difference of $408 per month ($4,896 a year)

The question is this:

Will you be able to invest the cost difference over the term of the 20-year term policy and end up with a $1 Million dollar balance after taxes?

Most comparisons I see don’t account for the “Income-Tax-Free Death Benefit”

Not only does your investment have to equal the death benefit but the invested difference has to equal a sum large enough to provide you with the same after-tax amount of the death benefit.

For this exercise, I’ll ask you to open up your favorite financial calculator and follow along with me!

The rate of return I’ll use for this exercise is 10%.

Please enter the cost difference of $408 per month for 240 months or 20 years with a 10% rate of return and let’s compare the numbers.

$408 per month with an all-in amount of $97,920 in total contributions…..

After 240 months at 10% the account balance would be $295,386.59.

If your calculator is providing you with the same number I got…Then *Houston We Have A Problem*

We need an after-tax balance of $1,000,000 however the before-tax and before-fee balance is only $295,386.59.

If we account for a 1% management fee the balance drops to $262,530.09

If we account for taxes and fees for your beneficiaries…. Let’s assume only 30%, the balance drops to an after-tax amount of just $183,771.06.

By simply investing the difference you are short by $816,228.94

************************

Earlier I said it was literally impossible to become self-insured by the end of your term life insurance policy by simply investing the cost difference between a cash-value policy and a term policy.

If you participated in this simple but important exercise, using YOUR calculator and not mine….

You will now understand why I made this very Factual Statement!

It’s literally impossible for you to be self-insured by the end of your term policy by simply investing the difference.

TRUST ME I GET IT!

I like the catchphrase too!

“Buy Term & Invest The Difference” it sounds really cool!

However, as cool as it sounds…. it’s very misleading, it’s very manipulative, and it’s not even close to being accurate!

The good news is this:

I don’t work for anyone!

I don’t have a company telling me I can only recommend Buy Term only & invest the difference.

No one tells me to only recommend Whole Life Insurance.

No one tells me to only recommend IULs.

No one tells me to only recommend annuities.

No one tells me to only recommend stock market portfolios.

No one tells me to only recommend company A versus company XY&Z!

I’m free to run by business how I see fit so if there is any Agent /Advisor/Guru who can show me the math, I’m on board!

Show me the numbers… This isn’t about me it’s about the clients, so if you can show me the numbers I’ll be on board with you!

However, when it comes to simply investing the cost difference between a cash-value life policy and a term life policy with the expectation of being self-insured by the end of the recommended 20-year term….. the math will never work!

*************************************

Myth Exposed* “Buy Term & Invest The Difference” = Annihilated!

************************************

Just in case you are interested…I decided to run the math on this strategy to age 80!

Simply investing the difference would take 38 years and 4 months just to break even!

But question? Are you guaranteed to live long enough just to break even?

Using the same numbers as above you’ll need an account balance of $1,428,571 to net $1,000,000 after tax. (30%)

The cost difference of $408 invested at 10% for 460 months (38 years 4 months) = $1,960,592.32

After the fund fee and mgr fee of 1.25% the balance is $1,427,917

After Taxes, the balance (30%) is $1,000,000.

Let’s take a look at a more realistic 360 view.

The person in this example is 42 years old.

Most advisors don’t recommend their clients maintain an aggressive high-risk portfolio in retirement, so in this example we’ll account for that.

From age 42 to 65 rate of return 10% at age 65 retirement rate of return 5%.

276 months to age 65 with $408 invested monthly at 10% with a fee of just 1.25 after mgr fees equal an account balance of $358,074.19

Starting at age 65 switch to a conservative account. 5.5% with the same small fee of just 1.25%

$356,805.78 grows to $1,423,239.70 before tax by age 93 and 3 months old, which should net $1,000,000 after tax.

You would be Age 93 before breaking even!

Assuming you don’t die before age 93….

This also assumes you don’t touch this money for retirement income!

Assuming you don’t touch this money for medical bills or other financial emergencies…

You’ll have to last 51 years plus until age 93 & 3 months just to break even!

Important Note:

If we have to account for long-term care insurance premiums….you will never break even.

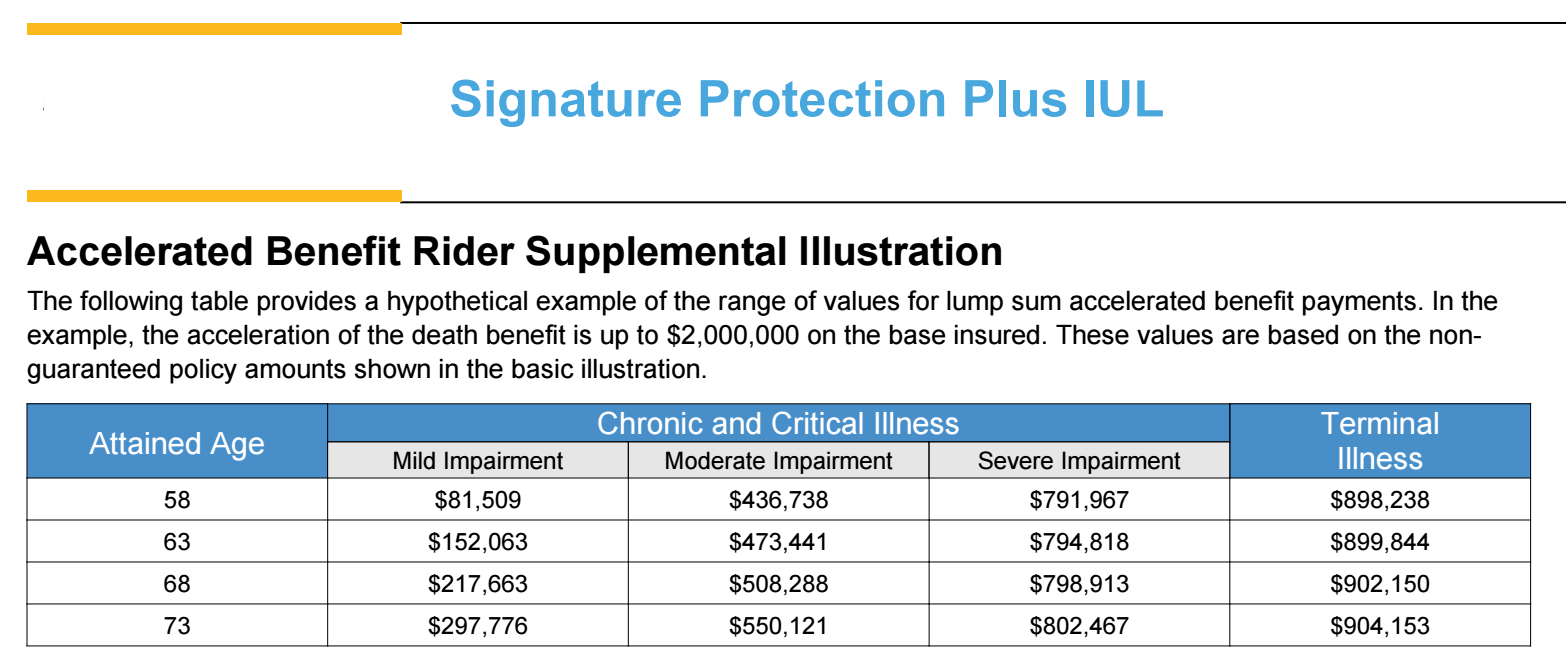

Please remember…the cash-value life insurance policy used in this example would provide you with $802,467 income-tax-free for long-term care services (by age 73) and $904,153 for Terminal illness income-tax-free!

If you purchase a long-term care policy at age 60 to age 90 it will cost you around $139,000 or $386.11 monthly average.

Subtract the invested difference of $408 (cost difference between the term & cash-value life) – $386 (which is the average cost of LTC premiums over 30 years from age 60 to 90) = a difference of just $22 you’ll have left over to invest each month for the next 30 years lol!

By age 93 your account balance would be $566,516.34 after taxes…almost a half million short.

It would take you until age 111 to break even after taxes.

I guess technically the answer is Yes!

It will work if you are guaranteed to live until age 111 and assuming you never touch the money!

So now you know the rest of the story with regards to Buy Term & Invest The Difference.

*Strategy Busted*

Cost of Insurance Is Too High When You Get Older?

***Newsflash***

All Life Insurance Plans –

Term Life Insurance

Whole Life Insurance

Universal Life Insurance.

All means All.

The Cost Of Insurance for every type of life insurance increases over time.

I like term insurance for particular situations however a pure term insurance policy over time will become the most expensive type of life insurance you can own!

Don’t believe me?

Open up your term life insurance policy illustration and flip to page 3, 4 & page 5.

Most term life illustrations are only 11 pages and typically the premium payments start on page 3.

Assuming you purchased a 20 year term policy with guaranteed level premiums for 20 years….. your policy illustration premium page will look just the picture below this section that says “Term-Illustration Page 1”

Notice the highlighted area in blue which shows the guaranteed level premiums.

With my example below the guaranteed annual level premium is $765 or $63.75 per month.

This is a 20-year term policy and the insurance company is capping the premiums for the first 20 years only…..however, if you have to renew this plan because you developed serious health conditions or for whatever the reason is:

Notice how the premium in year 20 is just $765 but the premium in year 21 jumps to a whopping $12,638!

Notice how these premiums continue to increase every single year!

By year 41 the annual premium is over $100,000

By year 55 the annual premium is almost $600,000!

The total premium for this 1 Million Term Life Insurance Policy to age 97 is an astounding $5,344,690!

That’s 5 Million plus….

Critiques of cash value life always talk about the cost of insurance reaching unbearable limits when you get older during a time you can least afford to have increasing premiums.

YES! They say your premiums will increase when you get older due to the cost of insurance increasing.

The funny part of this argument is this:

***They’re actually explaining what will happen to your term life insurance if you find yourself in a situation needing to renew it. lol! They’re just clueless and don’t know it!

Insurance companies are required by law to include these “minor premium increases” as part of your term life policy illustration.

However, 99.99999999% of Agents / Advisors selling term life only, never explain this part of the illustration to you.

If you find yourself uninsurable by the end of your initial term period & you still need coverage – you are screwed*

There is no way the vast majority of Americans will be able to afford a one-year renewal period not to mention the policy renewing for an additional 20 – 30 years.

89% of Americans 65 and older are on some kind of prescription medication.

Are you understanding what this means?

The majority of Americans with term policies ending right before or after turning age 65 will face the reality of not qualifying for life insurance at a reasonable price due to health conditions.

Currently, 91.2544% of all Americans over the age of 65 still find themselves needing life insurance.

70% of Americans 65 and older will need long-term care services.

For whatever reason the “Buy Term Only Crowd” is perfectly ok with leaving you & your beneficiaries in a messed up financial situation later on in life.

Their not interested in planning for the “What If”!

They know its much easier to get 1,000 people paying $20 per month…much easier to get a quick hit moving on to the next person without caring about the “What If”

There are a lot of what-ifs when it comes to buying term only & investing the difference however there are no “What If’s” when it comes to a “Permanent Cash Value Life Insurance Policy with “Guaranteed Premiums” for life!

My favorite IUL is my favorite cash value life insurance policy. With this IUL the premiums are guaranteed up to age 121.

The premiums are guaranteed to never go up!

If your family life expectancy is only 89 I can lower the premiums of this plan by lowing the premium guarantee to age 96!

The starting premium for the cash value life insurance policy is much higher than the starting premium for a term life policy.

The 1 Million Term Life policy in this example starts off at $765 per year but if you need this coverage beyond 20 years until age 96 the total premiums paid will be over 5 Million…$5,344,690!

The cash-value life insurance premium starts off at $5,651 per year. If by year 20 or by year 25 you decide you no longer need the coverage you can get 100% of your money back.

Or you can continue the coverage until age 96 without a premium increase.

$5,651,690 (Term Life)

versus just

$310,805 (Cash-Value Life-Permanent).

It’s not even close! The Permanent Life Insurance Policy is the clear winner!

The next question you might be thinking is…

How are the permanent life insurance premiums guaranteed, if the cost of insurance for all life insurance plans increases over time?

Great question, let me explain!

Continue to Part 2.

Part 2: Cost of Insurance Is Too High When You Get Older?

Whole Life Insurance was the “Original” Buy Term & Invest The Difference!

This concept wasn’t started by AL Williams aka Primerica!

This concept was started by Insurance companies looking to reduce the cost of insurance over time.

A whole life policy or any cash-value life policy is nothing more than a “Term Policy” with an interest account attached.

This is why the cost of insurance for “All Types Of Life Insurance” increases over time.

The interest account or cash value is what helps to keep the cost of insurance lower in later years so much so that insurance companies can guarantee your premiums over the “LIFE OF THE PLAN” when attaching term insurance to an interest account.

This Insurance Company Strategy is the very same thing the “Buy Term Only & Invest The Difference” strategy tries to mimic! But they can’t!

Insurance companies are some of the world’s best investors.

Insurance companies not only use the cash value to help reduce the cost of insurance over time…they also use “Risk Pooling”(

Individual investors don’t have access to “Risk Pooling” which plays a major role in helping to contain the cost of insurance over time.

(fyi Side note: This is the same reason why annuities can provide you with a higher payout guaranteed for life versus the same equivalent account balance via a market portfolio)

*Risk Pooling – Mortality Credits*

Buy Term & Invest The Difference is almost the equivalent of someone claiming they can “Time The Market”

There is no way under normal circumstances you can purchase a term policy & invest the difference with the expectation the invested difference will equal the original death benefit by the end of the original term.

It’s not going to happen! The math is not on your side.

Recap:

The interest accounts attached to term life insurance is what makes it a whole life insurance or permanent insurance.

When you look at a term life illustration you’ll see gigantic increasing premiums during the later years because there was never an interest account attached to help keep the cost of insurance in check….

When you look at a “Whole Life or Permanent Life illustration you don’t see this because the interest account helps in keeping the cost of insurance in check.

Yes, the premiums are higher because of the need to earn a rate of return (investing the cost difference) along with risk pooling!

The premiums are higher from the beginning to help spread the risk of earning a higher rate of return over time!

The benefit of this is clear.

In return for having this interest account attached to your term life policy, the insurance company can guarantee your premiums for life and they can guarantee your death benefit for life.

Not only are insurance companies some of the best investors in the world but also the best at predicting mortality.

Term Life Insurance is also used to help pay for the cost of insurance over time…

Think about it!

100% of all permanent life insurance policies will receive a payout.

Less than 1% of all term life insurance policies will receive a payout.

Insurance companies know this!

All the premiums you pay for term life insurance are added to the risk pooling side of things to help pay for the life insurance coverage they’ll actually end up paying for lol.

So YES!

The cost of insurance goes up drastically…But, with term life insurance, but the premiums you pay for 99.99999% of whole life / Permanent premiums can be guaranteed for life.

Question: The Evil Insurance Company Keeps Your Cash Value When You Die? True Or False?

I will explain this part by providing the transcript to a conversation I was having with an Investment Advisor / Agent.

*****

How “Cash Value Life Insurance Works”

If you don’t have the money or credit to secure a $500,000 loan to purchase an item….and a 3rd party agrees to secure the loan on your behalf.

You must agree to pay $250,000 cash today along with the remaining $250,000 cash paid in 1 year.

The 3rd parties NAR or Net Amount At Risk for this $500,000 loan is only $250,000 because you’ve already paid $250,000!

A year later when it is time for you to pay the remaining balance of $250,000 you go missing. The 3rd party lender can’t find you.

How much did the 3rd party lender lose in this scenario?

$500,000 or just $250,000?

If you said the total loss was just $250,000 (The NAR-Net Amount At Risk) you are a genius!

Truth be told… this is the way it works with every loan (but with interest added lol)

WAIT@!$

What if you paid $250,000 upfront cash and you also secured a $100,000 bond as additional collateral for just in case you default on the loan?

As fate would have it this individual also goes missing.

The 3rd party lender then secures access to your $100,000 bond collateral.

How much did the 3rd party lender lose in this scenario?

$500,000 / $350,000 / $250,000 or $150,000?

If you said the total loss was just $150,000 (The NAR-Net Amount At Risk) you are now an executive genius! lol

The 3rd party lender was already paid $250,000 plus they took control of your $100,000 bond collateral with a remaining balance of $150,000 owed or short!

The NAR -Net Amount At Risk in this scenario is just $150,000!

*********************************

If you get this next question right you will become the “LI Jedi Master” lol

The Scenario:

You want to leave $1,000,000 as an inheritance to your children!

The only problem is, you don’t have a million dollars sitting in your bank!

A co-worker tells you about a company willing to pay your children a million dollars if and when you die.

You ask, what’s the catch?

Glad you asked!

They will actually allow you to make payments towards the one million dollars you want to leave to your children.

If something happens to you before you pay off this million dollars, they will pay the difference.

In other words, if you’ve only paid $100,000 towards this million-dollar inheritance….. this company will still pay your beneficiaries the entire $1,000,000!

How cool is that?

The $900,000 you didn’t pay will be added to the $100,000 you’ve already paid, and your children will receive the entire 1 million balance.

So now here’s the question?

If this person dies after only paying $100,000 towards the 1 million balance.

How much money did this company lose?

$1 Million / $100,000 or $900,000?

If your answer is $900,000 you are now an “LI Jedi Master”

Now!

What if the $100,000 you paid, earned a rate of return that grew the account balance to $700,000?

Even with this growth the $700,000 doesn’t cover the entire 1 million balance, you are still short $300,000.

Remember, you want to leave 1 million (not $300,000 not $100,000, not $700,000) You want to leave 1 million.

But the good news is this:

Even though your total account value is less than the 1 million owed…. this company will still pay your children the entire 1 million balance or will they?

Question: At stake is the “LI Jedi Grand Master” Title.

What amount will the children receive?

A) Will they only receive the $100,000 you paid?

B) Will they only receive the $600,000 interest earned?

C) Will they only receive the $100k paid along with the $600k interest for a total of $700,000?

OR

D) Will they receive the $100k paid along with the $600k earned interest along with the $300k you didn’t pay… for a grand total of $1,000,000?

If your answer is D…. They will receive the $100,000 you paid along with the $600,000 earned interest and they will also receive the unpaid portion of $300,000 for a grand total of $1 Million!

If this is your answer…Congratulations, you are now an “LI Jedi Grand Master” lol!

For extra credit…

The follow-up question is this.

In this scenario how much money did the company lose?

A) $1 Million?

B) $100,000?

C) $600,000?

D) $700,000?

OR

E)Just $300,000?

If your answer is (E), you are the extra credit superstar!

$100,000 was paid by the person!

$600,000 was the interest earned!

Which leaves an unpaid balance of $300,000!

Common sense stuff right?

************************************

If this was easy for you to understand, please give me 5 Stars lol!

I need 5 Stars only!

I need you to be 100% completely satisfied.

“Common Sense Stuff Can’t Get Any Easier”

If this was easy for you to understand, “YOU” “NOW” (Finally!!!) understand, how “Cash Value Life Insurance Works”

(With option B it’s +++)

Soooo!

If you have a $1,000,000 cash value policy with a $700,000 cash value balance….. How much life insurance are you actually paying for?

The answer is $300,000 because $700,000 is already accounted & paid for… by way of premiums paid plus interest earned – cash value!

$300,000 is the unpaid balance!

Now Give Me 5 Stars!

*******************************************************************

What if it’s a Term Policy?

If you have a 100,000 25-year term life policy with a premium of $100 per month.

After paying on this policy for 20 years….. the total paid would equal $24,000.

If you died after making the 240th payment ($24,000)

#1. How much does the Insurance company have to pay to your beneficiaries?

#2. Does the insurance company pay your beneficiaries the $100,000 death benefit along with the money you paid into the policy… for this example $100,000 plus $24,000 for a total of $124,000?

#3. Or does the insurance company only pay you the “NAR” Net Amount At Risk? Which equals the death benefit minus what you paid? For this example, the net amount of risk equals $76,000?

#4. Or does the insurance company pay your beneficiaries the “NAR” ($76,000) plus the premiums paid ($24,000) for a total of $100,000?

The answer is #4 – $100,000!

******************************************************************************

Fyi.. This info is “Insurance Basics 101”

If you hold a Life Insurance license….

(This info was a part of your certification)

I’m providing you links to life insurance exam questions about cash value life and what happens to the cash value.

These are links from sources that teach the life insurance licensing exam.

This is also in line with Investopedia’s explanation which I also provide below:

Below is a link from.

SEC.gov

Investopedia

Quizlet.com (licensing exam)

brainly.com (licensing exam)

Study.com (licensing exam)

Flash Cards Cash Value Life

https://quizlet.com/768339970/flashcards

Pauline, age 45, would like to purchase life insurance. She wants a policy that will provide lifetime protection, and she would like to build up a cash value. Pauline has a low risk tolerance and wants the cash value to be invested in the insurance company’s general account. She wants the insurance company to assume all the investment risk for the cash value, and she wants a policy that guarantees a minimum cash value at each age. Which of the following policies would best meet Pauline’s needs?

Pauline, age 45, would like to purchase life insurance. She wants a policy that will provide lifetime protection, and she would like to build up a cash value. Pauline has a low risk tolerance and wants the cash value to be invested in the insurance company’s general account. She wants the insurance company to assume all the investment risk for the cash value, and she wants a policy that guarantees a minimum cash value at each age. Which of the following policies would best meet Pauline’s needs?

A)

Variable universal life

B)

Term life

C)

Whole (ordinary) life

D)

Variable life

The whole (ordinary) life policy best meets Pauline’s needs because it will provide protection for her entire life (if the premiums are paid as agreed) and a guaranteed cash value. In addition, the insurance company assumes all of the investment risk and guarantees a minimum cash value at each age.

***********************************************

This is another licensing exam course!

brainly.com/question/31859771

Expert-Verified Answer

No one rated this answer yet — why not be the first? 😎

shreyabansal842

Ambitious

11.9K answers

1.5M people helped

Final answer:

In an Ordinary Whole Life Insurance Policy, the net amount at risk decreases over the life of the policy.

Explanation:

In an Ordinary Whole Life Insurance Policy, the net amount at risk will typically decrease over the life of the policy. This is because as the policyholder makes premium payments over time, the cash value of the policy increases, reducing the net amount at risk for the insurer.

For example, let’s say a policyholder initially purchases a whole life insurance policy with a death benefit of $500,000. In the early years of the policy, the net amount at risk may be close to the full death benefit, as the cash value is still low. However, as the policyholder continues to make premium payments and the cash value accumulates, the net amount at risk decreases.

By the time the policy reaches maturity or the insured individual reaches a certain age, the net amount at risk may be minimal or even zero if the policy has built up sufficient cash value. This means that the insurer is no longer exposed to a significant risk of having to pay out the full death benefit, as the policyholder has essentially prepaid a portion of it through premium payments.

****************************************************

Let’s see what SEC.Gov says…

SEC.GOV

https://www.sec.gov/resources-for-investors/investor-alerts-bulletins/ib_varlifeinsurance

Look under: How Variable Life Insurance Works

Variable life insurance is a form of life insurance. Like other life insurance, it provides a death benefit that may be significantly larger than the amount of premiums you pay.

With a variable life insurance policy, you will be required to pay premiums into an account. The amount of the premium payments that go into the account may be less than you paid because fees were taken out of the premium payments. The money in the account gets invested in a menu of investment options—typically mutual funds— that you can select.

In addition, you may be able to allocate part of your premiums to a fixed account. A fixed account, unlike a mutual fund, pays a fixed rate of interest. The insurance company may reset this interest rate periodically, but it will usually provide a guaranteed minimum (e.g., 3% per year).

The money in your account will vary according to the amount of premiums you pay, the amount of policy fees and expenses, and the performance of the investment options you choose.

Example: You purchase a variable life insurance policy with an initial premium payment of $100,000. You allocate 50% of that payment ($50,000) to a bond fund, and 50% ($50,000) to a stock fund. Over the following year, the stock fund has a 10% return, and the bond fund has a 5% return. At the end of the year, your account has a value of $107,500 ($55,000 in the stock fund and $52,500 in the bond fund), minus fees and expenses (discussed below).

Your policy may require you to pay a specified amount of premium payments or provide you the flexibility to pay varying premiums as long as you contribute enough to pay your policy fees and expenses.

Some policies may also provide protection from lapse (that is, not having sufficient policy value to pay your policy fees and expenses) if you pay in a certain level of premiums. A policy may lapse if there is not enough cash value (either as a result of policy fees and expenses or poor investment performance or loans) to pay the current policy fees and expenses.

(Here WE GO)*****

The more money you pay in premiums, the lower some of your policy’s fees and expenses may be. This is because your net amount of risk determines some policy fees and expenses. Your net amount of risk is the difference between your policy’s face amount and your policy’s cash value, so it goes down if there is more money in your account.

Also see: Investopedia:

https://www.investopedia.com/terms/a/amount-at-risk.asp….

What Is Net Amount at Risk?

The net amount at risk is the monetary difference between the amount of money paid out for a life insurance policy and the accrued cash value paid for it by the insured individual. The net amount at risk number is critical to insurance companies as it represents how much of the policy has been paid for before it has to be distributed, which impacts the profitability of the company and how it manages its reserve balances.

Key Takeaways

- The net amount at risk is the difference between the death benefit paid out on a life insurance policy and the accrued cash value paid for it by the insured.

- The net amount at risk is highest in the early stages of a life insurance policy and decreases as the insured increases in age.

- The net amount at risk exists until a policy has been fully paid up.

- If the net amount at risk needs to be paid out, the loss is covered by an insurance company’s statutory reserves.

****************************************

I’ve just provided you with 3 different licensing exam questions along with an explanation from “SEC.GOV & Investopedia… You literally have no excuse for continuously repeating the same misinformation!

SEC.gov

Investopedia

Quizlet.com (licensing exam)

brainly.com (licensing exam)

Study.com (licensing exam)

************************************

The answer is NO*

The Evil Insurance Company doesn’t keep your cash value, after all, you are purchasing something you most likely will never fully pay for.

YES! You are actually paying for something

It’s not a free loan!

****************************************

Congratulations, you now can explain how cash-value life insurance works better than the majority of advisors and agents who sell it or sell against it.

The interest account or cash value helps to control the cost of insurance in later years, this same interest account also helps to reduce an Insurance company’s “NAR” Net Amount At Risk!

When talking about an IUL. The ART’s Annual Renewable Term does increase each year however please don’t confuse this with the overall cost of insurance which actually decreases over time.

Why?

Again it’s about the “NAR”

If you start off with a $1 Million policy on day one the total risk to the insurance company is $1 Million and you start off paying for $1 Million in coverage.

If after 30 years the account accumulation value /cash value is $700,000…. you are no longer paying for $1 million in coverage, you are only paying for $300,000 of life insurance because the account value is $700,000 and if you die the unpaid balance isn’t 1,000,000 it’s just $300,000….the Net Amount At Risk!

And your beneficiaries receive both the account value/cash value (The $700,000) and the Net Amount At Risk ($300,000) to combine for the total death benefit in this example of 1 million.

Question: The Evil Insurance Company Keeps Your Cash Value When You Die? True Or False?

False?

Do you need life insurance after 65?

A very popular social media influencer made this comment:

“The VAST majority of people don’t need a permanent life insurance policy aka “cash-value life” Instead purchase a 20-year term policy and make sure you purchase one that allows you to renew it” Just in case you still need coverage and your health takes a turn for the worst.”

Important Note:

I’ve already annihilated the quote about picking a term policy that allows you to renew just in case your health takes a turn for the worst.

This is the worst advice ever. Clearly, this person has never looked at a term life insurance illustration.

Term Life Insurance plans are cost-prohibitive when entering the renewal period.

99.99999% of Americans will never be able to afford a term life insurance policy renewing to age 95 and beyond!

Next, if you might need coverage due to declining health in later years….. It couldn’t be any more obvious which type of coverage you should pick. (Permanent)!

Next, this person actually said… “The VAST majority of people don’t need a permanent life insurance policy”

When viewing this person’s video it’s clear no research was done at all.

By the way this person is 27 years old and after listening some more I’m sort of under the impression the message was more geared toward people in their 20s and early 30s but at the same time they kept repeating the “Vast Majority Comment”

After challenging this person on these comments I did ask for clarification on what the “Vast Majority” is!

I’m still waiting for an answer!

However, it’s a valid question!

Can the “Vast Majority Of People” go without a permanent life insurance plan?

If you’ve been following along in my previous segments, I’ve already laid out the case for permanent life insurance.

I decided to provide you with a demographic and informational outlook resource to check out.

******

Demographic Outlook

https://www.cbo.gov/publication/59899

By 2040, with the aging of the population, deaths exceed births in CBO’s projections

Older Americans face a caregiving gap, especially those with lower incomes and dementia.17 Demand for elder care is expected to increase sharply with a rise in the number of Americans living with Alzheimer’s disease, which could more than double by 2050 to 13 million, from 6 million today.18

Alzheimers Association

https://alz-journals.onlinelibrary.wiley.com/doi/10.1002/alz.13016

Social Security and Medicare expenditures will increase from a combined 9.1% of gross domestic product in 2023 to 11.5% by 2035 because of the large share of older adults.19

Federal budget cuts and tax increases may be inevitable as more members of the large baby boom cohort reach retirement age and become eligible for entitlement programs. Policymakers can invest resources today to reduce poverty and improve the economic outlook for workers. These investments can increase young workers’ future productive capacity and help offset the costs of an aging population.

56.91 Million between 20-44 Men

66.75 Million between 20-49 Men

54.99 Million between 20-44 Women

64.77 Million between 20-49 Women

Men & Women 20 – 49 131.52 million

50 and older 115 million.

81.07 Million 19 and younger..

Age 20 to age 44 111.9 million

45 and older 140.9 million

79.01 Million 60 and older

57.89 Million 65 and older..

https://www.statista.com/statistics/241488/population-of-the-us-by-sex-and-age/

The Joint Center for Housing Studies of Harvard University found 41% of homeowners 65 and older had a mortgage in 2022, compared with 24% in 1989. Among homeowners 80 and over, the percentage with mortgages rose from 3% to 31%.

The amounts owed have skyrocketed as well. Median mortgage debt for those 65 and older rose more than 400%, from $21,000 to $110,000 (both figures are in 2022 dollars). Median mortgage debt for those 80 and over increased more than 750%, from $9,000 to $79,000.

https://www.jchs.harvard.edu/press-releases/older-adult-population-soars-us-unprepared-provide-housing-and-care-millions-people

https://data.census.gov/table/ACSDT1Y2022.B25027

****************************************

It’s been said that by the year 2046 67% of homeowners 65 and older will still have a mortgage.

****************************************

Long-Term Care

The Joint Center for Housing Studies of Harvard University found…

The Cost of Long-Term Care Is Out of Reach for Most Older Adults

The costs of long-term care (LTC) services are also high, averaging over $100 per day nationwide. The majority of older adults will need these services and those with very low incomes, who are most likely to require them, have the fewest resources to pay for them. When LTC services are added to housing costs, only 14 percent of single people 75 and over can afford a daily visit from a paid caregiver, and just 13 percent can afford to move to assisted living.

https://www.jchs.harvard.edu/press-releases/older-adult-population-soars-us-unprepared-provide-housing-and-care-millions-people

Student loan debt is expected to be a problem for an increasing number of retirees in the future, too. Some 3.5 million people over the age of 60 have more than $135 billion of student loans .5 Over the past 20 years, student loan debt held by senior citizens has increased 19-fold — either the remnants of their own loans or loans co-signed for children or grandchildren.

https://www.newyorkfed.org/microeconomics/topics/student-debt

If life insurance was only about having enough money to pay off your debt as this social media influencer was suggesting…. A lot of people are going to be in trouble.

31% of individuals over the age of 80 as of 2022 still have a mortgage!

A home that cost a modest $200,000 20 years ago now costs $428,000!

When I purchased my first new car at the age of 19 the average loan term was 36 to 48 months with an average payment of $250.

Today an average payment is $550 an average loan term is almost double at 72 months with some 84-month terms.

The same thing is going to happen with home loans and the result of this will lead to even more people over the age of 80 with a mortgage.

By the year 2044 66% of individuals over the age of 80 will still have a mortgage.

After viewing the research from credible sources, it doesn’t look like the vast majority of people will be debt-free in retirement.

Also, the rising cost of health care in retirement is certainly outpacing the average investment returns expected in retirement.

Without a permanent life insurance plan in retirement that can double as long-term care coverage or critical illness coverage, you’ll find yourself stuck having to dig deep into your fixed-income retirement accounts and therefore triggering an irreversible income deficiency.

Will you run out of money before you run out of life?

Asset protection life insurance can help protect your retirement income from future health decline!

It’s much cheaper for Insurance to cover the cost instead of you reaching into your fixed income sources to cover the cost, but either way, these costs are coming! Ready or Not!

SO –

Even if you don’t max-fund a cash-value life insurance for retirement income….. having a cash-value life insurance will still save you a boatload of money during retirement even if you are making premium payments into retirement.

The Joint Center for Housing Studies of Harvard University found…

The Cost of Long-Term Care Is Out of Reach for Most Older Adults

The costs of long-term care (LTC) services are also high, averaging over $100 per day nationwide.

The majority of older adults will need these services and those with very low incomes, who are most likely to require them, have the fewest resources to pay for them.

When LTC services are added to housing costs, only 14 percent of single people 75 and over can afford a daily visit from a paid caregiver, and just 13 percent can afford to move to assisted living.

https://www.jchs.harvard.edu/press-releases/older-adult-population-soars-us-unprepared-provide-housing-and-care-millions-people

According to the Joint Center for Housing Studies of Harvard University….

Only 14% of current retirees are able to afford a Long Term Care Policy.

A Whopping 86% of current retirees are facing a “Long-Term Care Crisis”

This Harvard University study found the overwhelming majority of “Current Retires” don’t have the money inside of their savings & investment accounts to cover long-term care…which by the way 70% of retires will need long term care.

“BUY TERM & INVEST THE REST” Rep/Agent are dooming Americans in retirement.

Retirees can’t afford Long-Term Care policies that’s why only 14% have a plan.

Most retirees can’t qualify for long-term care due to health conditions later on in life.

Currently, 89% of all individuals 65 and older are on some kind of prescription drug.

Popular so-called Financial Gurus preaching buy term only say to wait until age 60 before purchasing an LTC plan….

Wait What!?@

Your advice is to wait until a time in your life when you’ll least be able to qualify for an affordable rate before getting a plan that will ultimately protect your retirement income.???

You are purposely dooming your fellow Americans with this bad advice.

How about this:

Purchase an IUL (Cash-Value Life) at age 30 with guaranteed premiums to age 105.

The premiums for a female at age 30 for $250,000 of coverage will cost $91 per month guaranteed for life.

This cash-value life insurance policy will provide a lump sum $200,000 income tax-free if long-term care services are needed.

A long-term policy purchased at age 60 (female) will cost on average $139,000 from age 60 to 90!

The IUL cash-value life insurance policy from age 30 to age 90 will only cost $65,520 guaranteed.

If at age 90 you die without needing the Long-Term Care Policy or services, your beneficiaries will receive nothing, Zip Nada Zilch… $ZERO dollars paid to beneficiaries from the long-term care policy.

If you die at age 90 with the cash-value life insurance policy without needing long-term care services, your beneficiaries will receive $250,000.

Option 1: pay $139,000 or more over 30 years for a plan that will only provide you with $4,555.55 per month for a maximum of 3 years (total $164,000 in ltc benefits)

But if you don’t need it and die the $139,000 you paid is gone.

Or Option 2:

Actually, have a plan in place by purchasing a Permanent Cash-Value Life Insurance plan you keep for your entire life by purchasing this plan at a very young age.

With this plan, you’ll literally save (Double the money)

And if you need to access this plan for long-term care services you can do so as a lump sum payment.

With this lump sum income-tax-free payment you could… (This is another High-Level Plan)

Keep $50,000 of the $200,000 for cash on hand to cover the first year of long-term care services.

For the remaining $150,000 you can purchase an Asset-based Long-Term Care Annuity with a 2.5X Multiplier held for one year.

With the 2.5x multiplier, the $150,000 in this annuity will turn into $375,000 used for long-term care purposes accessed income-tax free.

And guess what… You don’t have to dip into your other retirement income… it’s protected with this strategy all thanks to the “Cash-Value Life Insurance – IUL Policy that you keep your entire life!

While also cutting your long-term care insurance premiums by 55%!

Don’t just push products or cool-sounding catchphrases such as “Buy Term & Invest The Rest”

How about actually putting a plan in place based on what actually happens in the “Real World”

Stop dooming people with these silly catchphrases because that’s all it is…. a silly catchphrase!

Education Is Key!

Cash Value Life Insurance Is The Only Investment You Need?

First I would like to say I don’t believe in one-size-fits-all.

Every day I recommend Term, WL & IUL.

The recommendation is based on the client’s situational need, not some catchphrase “Buy Term & Invest The Difference”.

If you are working with an Advisor, Agent or TV & Radio Financial Guru and they use phrases such as “Only Do This” you should never contact them or listen to them again. (Forgive me for saying this last part…. I had a temporary flashback to what the “Only Crowd Says” lol.

When someone says:

1. Only buy term & invest the rest

2. Only Whole life

3. Only IUL

4. Only 401k

5. Only Mutual Funds

6. Only ETF’s

7. Only IRA’s

8. Only Stocks

9. Only Bonds

10. etc etc etc etc

11. When someone tells you to use a cash value life insurance for high-ticket items such as purchasing a car instead of using a bank????

12. When someone tells you to use a whole life policy like a bank????

13. When someone tells you to fund an IUL (Instead of) funding a 401k 1st.????

14. When someone tells you an IUL is the new Super Roth or Rich Mans Roth????

15. When someone all but guarantees you’ll earn 12% or more in the stock market every year in retirement???

16. When someone tells you 8% is a safe withdrawal from a market portfolio in retirement????

17. When someone says you don’t need a permanent life insurance policy when you get older????

18. When you are told a cash value life ie Whole Life or IUL is the only “Investment You Need” – Dont walk away…Run!

**************************************

I’m going to cut this list short but just know there are many more “Only(s)”I can add.

All of the above products have a place for someone.

It doesn’t have to be a one-size-fits-all mentality.

Just because a product isn’t a good fit for you doesn’t mean it’s not a good fit for the other 341,998,344 Americans lol.

It’s rare for people who make exclusionary recommendations to consider things outside of their bubble especially when money is involved, especially when a perceived threat to their current or future income is lingering. Or when their need to be “RIGHT ALL DAY EVERYDAY ALL THE TIME” is driving their secret agendas lol.

I don’t work for anyone! I don’t have a company telling me I can only recommend Buy Term only & invest the difference. No one tells me to only recommend Whole Life Insurance. No one tells me to only recommend IULs. No one tells me to only recommend annuities. No one tells me to only recommend stock market portfolios. No one tells me to only recommend company A versus company XY&Z!

I’m free to run by business how I see fit so if there is any Agent /Advisor/Guru who can show me the math, I’m on board!

Financial product recommendations should be about the client’s particular need not about your cool-sounding catchphrase!

Guaranteed Cash-Out

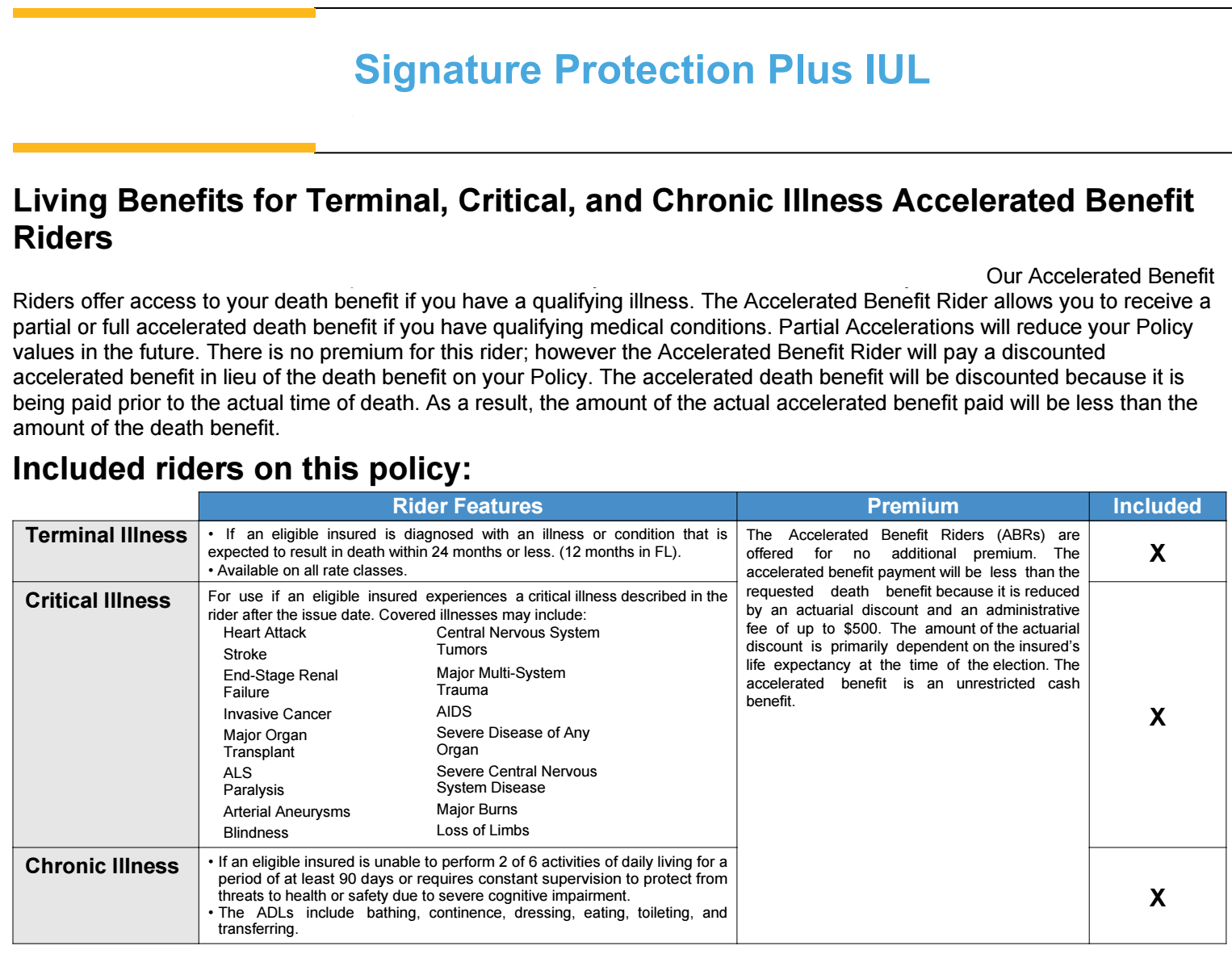

Living Benefits Rider

Living Benefits Details

Guaranteed Premium To Age 96

Term -Premium Page

Term- Illustration Page 1

Term- Illustration Page 2

Term- Illustration Page 3

I said earlier: I sell IULs not for what they might do…but for what they are contractually guaranteed to do! My strategy for annuities is the same.

I have one IUL for Asset Protection Purposes guaranteed to last my entire life. I have another IUL for cash-value growth for tax-free retirement income.

For cash value growth this policy only represents 15% of my total portfolio.

I’m a major advocate of max-funding a cash-value life insurance policy (whole life or IUL) however it shouldn’t make up your entire portfolio.

Many of the world’s brightest Financial Minds advocate for replacing the bond portion of your portfolio and replacing it with cash value life and annuities.

This is exactly what I’ve done with my portfolio as you can see below.

Does growing money in a cash-value life insurance & annuity work?

Ask Dr. Wade Pfau and others!

- Stock Market Growth Account 60%

- MYGA – Multi-Year Guaranteed Annuity 30%

- IUL Max-Funded Cash Value Life 10%

Academic scholars such as:

Dr. Wade Pfau Ph.D:

PhD, CFA, RICP® is the founder of Retirement Researcher, an educational resource for individuals and financial advisors on topics related to retirement income planning. He also serves as a principal and the director of retirement research for McLean Asset Management. He also serves as a Research Fellow with the Alliance for Lifetime Income and Retirement Income Institute. He is a professor of practice at the American College of Financial Services and past director of the Retirement Income Certified Professional® (RICP®) designation program.

He holds a doctorate in economics from Princeton University and has published more than sixty research articles in a wide variety of academic and practitioner journals. His research has been discussed in outlets including the print editions of the Economist, New York Times, Wall Street Journal, Time, Kiplinger’s, and Money magazine.

Wade is a past selectee for the Investment News Power 20 in 2013 and inaugural 40 Under 40 in 2014, the Investment Advisor 35 list for 2015 and 25 list for 2014, and Financial Planning magazine’s Influencer Awards. In 2016, he was chosen as one of the Icons and Innovators by Investment News. He is a two-time winner of the Journal of Financial Planning Montgomery-Warschauer Editor’s Award, a two-time winner of the Academic Thought Leadership Award from the Retirement Income Industry Association, and a Best Paper Award winner in the Retirement category from the Academy of Financial Services. Wade served for four years as a coeditor of the Journal of Personal Finance.

Wade has contributed to Forbes, Advisor Perspectives, and as an Expert Panelist for the Wall Street Journal. He has spoken at the national conferences of organizations such as the CFA Institute, the CFP Board, the FPA, NAPFA, and the Academy of Financial Services.

He is also the author of four books in the Retirement Researcher’s Guide Series.

Dr. Michael Finke, Ph.D. is a Professor of wealth management and Frank M. Engle Distinguished Chair in Economic Security Research at The American College of Financial Services. He received a doctorate in consumer economics from the Ohio State University in 1998 and in finance from the University of Missouri in 2011. He led the Retirement Planning and Living Consortium at Texas Tech University before moving to the American College, and is a nationally known researcher in the areas of retirement income planning, retirement spending, life satisfaction, and cognitive aging. He is a frequent speaker at financial planning conferences and was named one of the 25 most influential people in the field of investment advising in 2020 and 2021 by Investment Advisor Magazine.

Dr. Robert C. Merton: Ph.D. MIT & Nobel Prize Winner 1997

DR. William F. Sharpe: Ph.D. Stanford & Nobel Prize Winner 1990

Dr. Olivia S. Mitchell: Ph.D. Wharton & Executive Director of the Pension Research Council

Dr. Bridget C. Madrian: Ph.D. Dean, Marriott School of Management at BYU & Former Professor At Harvard & Chicago

Dr. David F. Babbel: Ph.D. Wharton & Former Professor at Berkley & A Division Founder At Goldman Sachs.

Dr. Moshe A. Milevsky: Ph.D. York University, Toronto

Dr. Mike Gallagher Ph.D.: Currently Part Of The ‘Trust Act’ Bi-Partisan Commission To Structure The Fix To The Trust Problems.

Also take a look at this BlackRock Study:

https://www.blackrock.com/us/individual/literature/whitepaper/how-to-optimize-retirement-income.pdf

Also see the Ernst & Young Report titled

“Permanent life insurance and deferred income annuities with increasing income potential outperform investment-only approaches in our analysis.”

In my opinion

Who Is A Candidate For Max-funding An IUL (Or WL)

Just like any financial product

Every warm body isn’t a good fit for every financial product lol.

Agents & Advisors are guilty of forcing everyone to wear the same size shoe!

*If the shoe fits wear it, if the shoe doesn’t fit still wear it*

1. Are you taking advantage of your employer’s 401k match?

If not, this is step #1 before trying to max-fund an IUL or WL.

2. As of 2024 if you earn under $161,000 single or under $240,000 as a married couple filing jointly you should be contributing to a Roth IRA up to the maximum amount of $7000 if under 50 $8,000 if 50 or older.

3. Have at least 10 months of income as an emergency fund already in the bank.

4. Pay off debt with interest rates of 6% or higher first.

5. You should already be following a financial budget.

6. Already be a member of some kind of fitness club that you attend on a weekly schedule.

Individuals committed to fitness every week without fail for whatever reason, tend to stick with their max-funded payment schedule above and beyond others who are not committed to some kind of fitness routine. (Don’t ask me why, I don’t know the answer)

7. After steps 1 – 6 are in order, at the absolute minimum have $416.66 per month you can contribute to an IUL for 20 years without ever missing a payment.

The ideal candidate is someone who can dump $20,000 per year into an IUL for 5 years!

Funding a Cash Value Policy works best when completed over 5 years.

With both these two scenarios, $100,000 is the total contribution. Scenario one completes the payments of 20 years while scenario 2 completes the payments over 5 years.

By age 70 scenario 2 will have $100,000 more cash value than scenario 1 even though both plans were funded with the same amount of money.

This is why properly funding the policy is very crucial to the overall success of the plan.

This is also why max-funding a policy isn’t for everyone!

If you are not financially stable & financially disciplined trying to max-fund any cash value policy will end up being a nightmare for you!

********************************************

The Scenario I typically see play out is someone stating a max-fund policy with a monthly premium of $100 – $200 per month with a death benefit of $250,000.

Newsflash***

This isn’t a policy designed for cash value growth! It’s barely enough to keep the policy in force till age 96 let alone have any kind of significant cash value accumulation.

This is an absolute no-go!

Unfortunately, all of the IUL TikTok Agents I come across are pushing IUL policy designs with premiums of $200 and under.

Little do they do they know, at some point in the future they might find themselves in a courtroom with their name on the door lol.

Most of the time when you hear stories of a cash value policy gone bad, its a result of bad policy designs.

I’ve given an example of 3 different policy designs for maximum cash value growth. Let’s review them again.

Scenario 1. $100,000 going into a policy with premiums spread over 40 years. The premium is $2,500 each year or $208 per month.

Scenario 2. $100,000 going into a policy with premiums spread over 20 years. The premium is $5,000 each year or $416 per month.

Scenario 3. $100,000 going into a policy with premiums spread over 5 years. The premium is $20,000 each year for 5 years.

Scenario 3 will have $100,000 more cash value than scenario 2.

Scenario 1 policy design will end up with a (negative cash value balance) In other words the policy will lapse after policy year 41.

You have to be financially stable & financially disciplined & the agent or advisor helping you has to know what they are doing.

Owning a cash value policy for maximum cash value accumulation might not be a good fit for you currently, however owning an IUL for Asset Protection & future long-term care benefits might be a good starting point for you today!

Half time show

Let’s Hear From Other Experts

Click Me Now To Purchase

![]()

The cash value of life insurance can be used as a buffer asset to help manage the sequence-of-returns risk exacerbated by taking distributions from a volatile investment portfolio

– Dr. Wade Pfau. –

![]()

Maintaining fixed distributions from investments in retirement increases exposure to sequence risk by requiring a higher withdrawal rate from remaining assets when their value declines.

– Dr. Wade Pfau. –

![]()

Temporarily drawing from the cash value of life insurance has the potential to mitigate this aspect of sequence risk for an investment portfolio by reducing the need to take portfolio withdrawals at inopportune times

– Dr. Wade Pfau. –

![]()

Dr. Wade D. Pfau, PhD, CFA, RICP® who holds a doctorate in economics from Princeton University and has published more than sixty research articles in a wide variety of academic and practitioner journals. His research has been discussed in outlets including the print editions of the Economist, New York Times, Wall Street Journal, Time, Kiplinger’s, and Money magazine. professor of practice at the American College of Financial Services and past director of the Retirement Income Certified Professional® (RICP®) designation.

![]()

Vist Dr. Wade Pfau’s website by clicking here.Visit

When you go to Dr. Pfau’s website make sure you start with “RISA”

Dr. Wade Pfau Ph.D:

PhD, CFA, RICP® is the founder of Retirement Researcher, an educational resource for individuals and financial advisors on topics related to retirement income planning.

He also serves as a principal and the director of retirement research for McLean Asset Management. He also serves as a Research Fellow with the Alliance for Lifetime Income and Retirement Income Institute. He is a professor of practice at the American College of Financial Services and past director of the Retirement Income Certified Professional® (RICP®) designation program.

He holds a doctorate in economics from Princeton University and has published more than sixty research articles in a wide variety of academic and practitioner journals.

His research has been discussed in outlets including the print editions of the Economist, New York Times, Wall Street Journal, Time, Kiplinger’s, and Money magazine.

Click on either image to review Dr. Wade Pfau’s educational books!

David McKnight Financial Advisor: is a renowned financial advisor and expert in zero-tax retirement planning, having assisted thousands of Americans in achieving the zero percent tax bracket.

He has frequently appeared in numerous national publications, including Forbes, USA Today, the New York Times, Fox Business, CBS Radio, and Bloomberg Radio.

With four #1 Amazon best-selling books to his credit, including “The Power of Zero”, Look Before You LIRP, The Volatility Shield, and Tax-Free Income For Life, David has established himself as a leading authority in retirement planning.

In his acclaimed book, The Power of Zero, he presents a comprehensive guide on how to achieve a 0% tax bracket in retirement through a carefully crafted, step-by-step approach.

Click on either image to review David McKnight’s educational books!

Ed Slott CPA & IRA Expert: is a nationally recognized IRA distribution expert, professional speaker, television personality, and best-selling author. He is known for his unparalleled ability to turn advanced tax strategies into understandable, actionable and entertaining advice. He has been named “The Best Source for IRA Advice” by The Wall Street Journal, and USA Today wrote, “It would be tough to find anyone who knows more about IRAs than CPA Slott.”

Mr. Slott is a Professor of Practice at The American College of Financial Services and regularly presents on IRA and estate planning strategies at both consumer events and conferences for financial advisors, insurance professionals, CPAs and attorneys, including virtual events drawing thousands of attendees nationwide.

Click on either image to review Ed Slott’s educational books!

Tom Hegna Retirement Expert:

When it comes to retirement, many consider Tom Hegna to be THE retirement income EXPERT! Tom is the author of three books, two whitepapers, and the host of the current Public Television Special, “Don’t Worry, Retire Happy!” which has aired in over 72 million homes since the debut in November 2014!

In his book “Pay Checks And Play Checks” Tom said…

If you ask 50 different financial advisors, you will get 50 different opinions about how to plan for a secure retirement. Their opinions are likely to be sub-optimal. Instead of offering you his opinion, Tom Hegna lays out for you the math and science behind a very simple retirement solution. It is so simple, that you will probably ask yourself, “Why doesn’t every financial advisor know this?”

Click on either image to review Tom Hegna’s educational books!

The Fees Are High

The Fees Are High Compared To What?

$20,000 For 5 Years

Death Benefit $394,668

Total Fees To Age 96

$66,878

$5,000 For 20 Years

Death Benefit $394,668

Total Fees To Age 96

$137,005

$3,500 For 29 Years

Death Benefit $394,668

Total Fees To Age 96

$423,950

Not All Cash-Value Policies

Are Designed For Maximum Cash Value Growth!

$20,000 (5 Years)

If using the plan for future retirement income…Funding the policy in 5 years will provide the best results. Funding the policy in 5 years will also result in drastically reduced fees.

With this properly structured policy the fees in the later years in relation to the cash value aren’t even 1% it’s only 0.23%

5,000 (20 Years)

If funding a policy over a longer period of time…As you can see with option two, it will work however you’ll cost yourself over $100,000 in cash value as you can see with this example. You could also end up with double the fees!

$3,500 (29 Years)

The premium paid isn’t high enough in relation to the death benefit to support building cash value and the policy will lapse by age 96 with no cash value.